How Owning a Home Builds Your Net Worth

Owning a home is a major financial milestone and an achievement to take pride in. One major reason: the equity you build as a homeowner gives your net worth a big boost. And with high inflation right now, the link between owning your home and building your wealth is especially important.

If you’re looking to increase your financial security, here’s why now could be a good time to start on your journey toward homeownership.

Owning a Home Is a Key Ingredient for Financial Success

A report from the National Association of Realtors (NAR) details several homeownership trends, including a significant gap in net worth between homeowners and renters. It finds:

“. . . the net worth of a homeowner was about $300,000 while that of a renter’s was $8,000 in 2021.”

To put that into perspective, the average homeowner’s net worth is roughly 40 times that of a renter’s. This difference shows owning a home is a key step in achieving financial success.

Equity Gains Can Substantially Boost a Homeowner’s Net Worth

The net worth gap between owners and renters exists in large part because homeowners build equity. When you own a home, your equity grows as your home appreciates in value and you make your mortgage payments each month. As a renter, you don’t have that same opportunity. A recent article from CNET explains:

“Homeownership is still considered one of the most reliable ways to build wealth. When you make monthly mortgage payments, you’re building equity in your home . . . When you rent, you aren’t investing in your financial future the same way you are when you’re paying off a mortgage.”

But on top of that, your home equity grows even more as your home appreciates in value over time. That has a major impact on the wealth you build, as a recent article from Bankrate notes:

“Building home equity can help you increase your wealth over time, . . . A home is one of the only assets that have the potential to appreciate in value as you pay it down.”

In other words, when you own your home, you have the advantage of your mortgage payment acting as a contribution to a forced savings account that grows in value as your home does. And when you sell, any equity you’ve built up comes back to you. As a renter, you’ll never see a return on the money you pay out in rent every month.

Bottom Line

Owning a home is an important part of building your net worth. If you’re ready to start on your journey to homeownership, let’s connect today.

Buyers: You May Face Less Competition as Bidding Wars Ease

One of the top stories in recent real estate headlines was the intensity and frequency of bidding wars. With so many buyers looking to purchase a home and so few of them available for sale, fiercely competitive bidding wars became the norm during the pandemic – and it drove home prices up. If you tried to buy a house over the past two years, you probably experienced this firsthand and may have been outbid on several homes along the way.

But here’s the news you’ve been waiting for: data shows clear signs bidding wars are easing this year.

According to the National Association of Realtors (NAR), the average number of offers on recently sold homes has declined considerably over the past few months (see graph below):

The graph shows homes were seeing a high of around five offers earlier this year. But the latest data shows that average was down to just shy of three offers per recently sold home. This shift is happening largely because rising mortgage rates moderated buyer demand and slowed home sales, resulting in a growing supply of homes on the market. Essentially, more choices for buyers.

What This Means for You

If you put your home search on pause because you were outbid last year or because you didn’t want to deal with the peak intensity of bidding wars, you can breathe a welcome sigh of relief. While it’s still a sellers’ market, an uptick in inventory gives you a window of opportunity to jump back in. You may still be competing with some buyers, but it likely won’t be anything like it was just a few short months ago.

Bottom Line

If you put your plans on pause because of intense bidding wars in recent years, it may be time to kick off your home search. Today, bidding wars are easing and that may mean less competition for you as a buyer. If you’re serious about buying a home or making a move, let’s connect to get started today.

Downsizing for Seniors

Downsizing is often the best option for seniors who want to cut costs or have medical problems requiring constant care. Selling their homes could provide them with additional funds to cover their retirement and other medical expenses. It also relieves them of managing a house, which in itself can bring stress and risk of accidents. There are many options available for senior care.

It is important that seniors understand their options to find a place best suited for their care needs and still allow them to thrive physically and mentally. Caring.com has created a few guides with an online directory to help seniors navigate the nearby assisted living facilities in California. Click the below links to learn more:

Here are the links for your quick reference:

Laura’s Neighborhood News – Back to School Supply Drive

How to Maintain a Good Credit Score

By Donny Gamble

Achieving a good credit score is often considered the hardest part of the credit process, however, once you reach a solid number, many people struggle to maintain their momentum.

To keep your credit score high, you need to be aware of how the credit score system works, and how your active spending influences the data.

Today we will explain the main factors which affect your credit score, methods to maintain your credit score, and tips to help you move from good to excellent.

Each of our suggestions can take a while to master, so remember that good financial security isn’t a race. Take your time, and be consistent.5 Factors That Affect Your CreditHow Lenders Use Your Credit ScoreWhat is a Good Credit Score?How to Maintain A Good Credit Score

7 Benefits of Having A Good Credit ScoreTips to Help Increase Your Credit ScoreMonitoring Your Credit ReportCredit Score FAQ’s

5 Factors That Affect Your Credit

There are 5 main factors that affect your credit score. They are your payment history, the amount you owe, the length of your credit history, your new credit lines, and the mixture of credit lines.

This may sound like jargon, but we will explain what these terms mean.

Payment History

Your payment history is often the biggest factor in determining your credit score. This category refers to your positive and negative payment history.

If you always pay your repayments on time, then your payment history will be positive. If you have fallen behind and were charged late payment fees, then this negative history will be remembered.

If you have filed for bankruptcy or collections, your payment history will show this record. After 6 years, your payment history expunges your record, meaning black marks against your name may be removed.

However, it can take 10 years for a bankruptcy notifier to be removed.

Balance

The second-largest factor is the amount you currently owe. If you are using all of your credit or going over your credit, then lenders will assume you are a risk.

This risk will lower your credit score. Most lenders will use a credit utilization rate to consider how much of a risk you are. They tend to want a rate of 30% or less.

They calculate the rate by adding up all of your credit lines (credit cards, loans, etc), and dividing them by the total credit limit currently offered to you (credit card max, overdraft max, etc).

They then multiply this number by 100 to create a percentage. You can figure out your own credit utilization rate using this method and see if you are under 30%.

Length of Credit History

The longer your credit history is, the more weight your claim of financial stability is. If you have never made a late payment in 20 years, your history shows you are capable of paying your monthly bills.

Whereas someone who has a 2-year long credit history still shows a possibility of risk. This is one reason why maintaining an old credit card is important to keep your score high.

New Credit Lines

Every time you apply for a new credit line (like a credit card or a loan), your credit score drops. This is because you are showing the need for more financial support.

People who apply for credit cards often receive a 0% ARP. Those in large debts often switch to these low APR rates so they can pay back their debt without interest.

Although this is a great way to reduce your debt, the credit score system recognizes that this is a sign of financial pressure.

Before you apply for a new credit card, ask yourself if the inevitable drop in your credit score is worth it.

Credit Mix

If you can show that you can successfully handle different types of credit lines (such as a mortgage, auto loan, student loan, credit card, store card, etc), then you are showing your ability to handle different financial responsibilities.

This concept is often the least important in the credit score process but is still a factor nonetheless.

How Lenders Use Your Credit Score

Lenders will use the score and the information above to consider how likely you are to pay back their credit. Although there are multiple different scoring systems, they all use this information but prioritizing different aspects of your credit history.

Each lender will use their own version of the calculation process, to show them how stable your financial situation is in comparison to their idea of importance.

What is a Good Credit Score?

Because each credit reference agency (the companies which score your credit) has a different method, there isn’t one number that indicates a good credit score.

Generally speaking, most agencies will rate you between 300 and 850. In this system, less than 580 is considered bad. 580 to 669 is often considered fair, meaning you aren’t in a great financial situation but you can keep on top of your finances.

670 to 739 often means you are doing well, but there is still a risk. 740 to 799 generally means you are doing very well but have the occasional negative impact (like applying for more credit).

Lastly, 800 and above is considered excellent. To be excellent you need to be stable financially, be living within your means, have a long history of good financial management, and aren’t considered a real risk.

How to Maintain A Good Credit Score

To maintain your credit score, you need to consider the factors above and keep showing lenders that you are not a risk. However, it is one thing to know that your credit utilization rate should be below 30%, but it’s another to understand how that works in your daily life.

To help you, we have created some tips and thinking points to help you maintain your good credit score.

Keep Credit Card Balances As Low As Possible

Although a 30% or less credit utilization rate is the goal, it will be easier to manage your rate if you keep your credit card debts as low as possible.

This simplified method will help you remember that as long as your credit card balance is low then your rate should be low too. Getting as close to $0 as possible will allow you to keep a high credit score.

Ideally, your credit card should be paid off every month. You could do this by paying off little bits every week and then clearing the debt at the end of the month, or you can ensure your credit only gets used to pay for things that you can afford to pay back instantly.

Pay Your Bills on Time

Because your payment history is the biggest factor in most credit scores, you need to pay your bills on top to maintain your good rating.

To make this task easier, we recommend automating your bills. Set your payment date for the second of each month (or the day after you get paid).

This way your bills will be taken out of your account before you have a chance to spend the money. As the payment will be automatic, you don’t have to worry about manually sending each company your money either – reducing your stress.

Some people find it easier to set up a bank account solely to pay their bills. They send the correct amount to this additional account, knowing they cannot accidentally spend the money.

The companies then take money from that account automatically on whichever date you can set up for them.

Do Not Close Old Credit Accounts

The longer we stay with a credit account, the more likely the APR will grow. New credit cards offer the best APR deals, but after a couple of years, the rates increase.

A lot of people close down their accounts when this change happens and search for a new account to get the best APR deals again.

Although this might seem like a smart move, when you close down an account you are closing the good payment history you have gathered.

We mentioned before that the length of your payment history is a key factor in your credit score. If you close down an account, that 20-year history which makes you look low-risk is closed down too – the data goes with it.

As long as keeping the account doesn’t harm your spending ability, you should keep your old accounts open to show off your payment history.

Limit Applications for New Credit Accounts

Following the same train of thought as our last point, you shouldn’t open a new account simply for the APR rate. Yes, you might want a lower interest rate, but ideally, you should be paying off your credit card debt at the end of the month. If you do this, you will not be charged.

This means it doesn’t matter what the interest rates are, if you are keeping your money under control, then you don’t need to look for the best rates.

As we said before, opening new credit lines suggests you need more financial support. It doesn’t matter if you are closing some down at the same time, as the rating system doesn’t take that into account.

You have to consider what is more important to you, maintaining a good credit score or having lower interest rates.

Check Your Credit Report Regularly

It can be easy to miss key information, especially when your life doesn’t revolve around your financial situation. If someone hacks your account, it can be a while before you realize the gravity of your situation.

Checking on your credit report regularly can help you spot unusual activity and question the situation before things take a turn for the worse.

You can then call up the company which has shown the fraudulent activity and explain the situation, saving your finances and your credit score at the same time.

Keep Track of Your Spending

For some people the bills aren’t the problem, it’s the small transactions that quickly start taking over their credit cards. Small transactions are just as significant as big ones, as they can seem like a non-issue that is easy to forget, but in reality, they take up your whole credit card bill.

Monitoring your own spending will allow you to see how much money you actually have left to spend, and can stop you from accidentally buying more than you can pay back.

We suggest figuring out how much money you half left after bills and then dividing that amount by how many weeks you have left until your next payday.

This amount becomes your weekly allowance. Count every dime you spend, and when a new week begins, you will have a new allowance to start over with.

Having small goals can help you manage your money and track your spending without too much pressure.

Do Not Exceed Your Credit Limits

As a general rule of thumb, you should never spend more than your credit limit. Although your lender may allow the transactions to go through, you will be charged for going over your maximum limit, and you will be telling your lender that you cannot follow their lending agreement.

This will show in your credit report, telling other lending companies that you cannot handle your finances.

Have An Emergency Fund

We used to say that everyone should have 3 months’ worth of their pay in their emergency fund. That way if they unexpectedly lose their job, they have 3 months to find a new one.

However, since the COVID-19 pandemic, we now know that 3 months isn’t long enough. The new goal is to have enough pay to sustain you for 6 months or more.

Not only does this show lenders that you have the financial security to pay them back, but it also protects you should you lose your job.

Pay What You Owe As Soon As You Can

Although you need to pay the minimum amount asked for by your lender before their due date, there is a better way to show you are good with money.

Paying little and often means that when the request comes, you’ll have already paid off their minimum requirement and then some.

Using the weekly allowance we discussed before, you could use any money not spent in the week to pay off your credit card.

Seeing as you will receive a new allowance in a few days’ time, paying off your credit card should not affect your plans in the weeks to come, but it will make reducing your debt easier.

7 Benefits of Having A Good Credit Score

Reading about the work you need to put in, might make you wonder if a good credit score is even worth it. To anyone kicking their feet and ready to give up, we want to show you how life can be easier and cheaper if you manage your credit score property.

Save Money on Insurance

When insurance companies consider your request, they look at your credit history. If they see that you struggle to pay your bills on time, they might charge you extra.

This is because you are seen as a financial risk, and so more money is needed to make sure that they have enough to cover your claims.

If your credit history and credit score show that you can pay your premiums on time, they will see you as a reliable customer. They will invest in your long-term membership with them, by lowering your charges.

Basically, if you can prove you can pay them on time, they won’t have to worry about receiving enough money, so they can afford to charge you less.

Save Money on Security Deposits

Some loans (like a mortgage) require a deposit before a lender will agree to the terms. The upfront payment ensures the lender still has some of their money, if you cannot keep up with the loan.

However, sometimes finding enough money to put down a deposit is too difficult. This in turn stops people from getting the mortgages or loans they need.

If you have a good credit score, you are showing the lender that you can keep up with your payments. This adds a level of stability to your application, suggesting that you are not at risk of financial instability.

Because of this, the lender may choose to offer a lower deposit request.

Save Money on Utilities

Just like insurance companies, utility companies consider your credit score when they offer you a fixed rate. A good credit score shows the company that you can pay them monthly, on time, and without issue.

Because you are less risky, they can charge you a lower amount knowing they don’t have to consider banking money for a possible future late payment incident.

Save Money on Cell Phone Services

Some cell phone companies require a deposit before agreeing to a phone contract. However, if you have a good credit score, you can avoid this large down payment and get a contract that doesn’t involve pre-paying.

Help Save Money on Interest and Fees

Interest rates on your credit cards are created using your credit score. Depending on what your score is, you may be entitled to a lower APR (annual percentage rate).

Just like with mortgages, and phone contracts, the lender is less worried that you won’t pay the money back and so doesn’t need to charge you as much.

As you are less likely to fall into a bad financial situation, the lender needs to create less of a safety blanket through the interest charges.

Get Approved for Higher Credit Limits

Because you have proved yourself capable of managing your finances, you are more likely to be approved for higher credit limits.

The better your credit score is, the easier it will be to apply for big loans, credit cards, and mortgages.

More Housing Options

Because you will be approved for higher credit limits and don’t need to pay as much in your deposit, your good credit score can help open your world to more housing options.

Although your income hasn’t changed, you have proven to the lenders that you can handle your current financial situation. With less money to pay upfront, larger loans to apply for, and lower interest rates, it all adds up to a larger home for you to purchase.

Tips to Help Increase Your Credit Score

If your credit score is good, but you want it to be excellent, or perhaps you are just a couple of numbers behind the green banner, then we have some tips to push you into the next credit score bracket.

Be Organized

The best way to increase your credit score is to be on top of your financial situation. This means knowing your monthly income, knowing when your bills are due, and tracking your spending habits.

You may need to cancel some subscriptions to keep yourself inside your spending limit, but if you can get to the point where you are saving every month instead of adding to your debts, then you are on the right track.

To go one step further, you can try and pay back your credit card debts strategically. The best method is to pay back every credit card’s minimum payment, but pay more to the least expensive account.

Once the least expensive account has been completely paid off, don’t add that monthly cost to your free-spending or savings account; instead, use it to pay off your larger debts.

This will create a snowball effect, allowing you to reduce your debts faster and faster with every credit account reduced to $0.

Consider A Credit-Builder Loan

A credit-builder loan is a small loan. The idea is to apply for the loan and to add a new credit line to your credit history. As we said before, one of the best ways to improve your credit score is to prove you can handle different types of financial borrowings, or “credit mix”.

Applying for a small loan, which you pay off in a couple of months, will add “loan” to the list of credit lines you can safely manage.

Which in turn, will make your credit history look even stronger.

Get A Credit Card

If you haven’t got a credit card already, we suggest that you get one. Although they may seem daunting, there is a simple way to use them without getting yourself into financial hardship.

Just as we discussed a weekly allowance earlier, you could use your credit card instead of your debit card to pay for your allowed spending.

Then when the week comes to a close, you can pay off the credit card using your debit card.

Become An Authorized User

If you need a quick boost to your credit score, then we suggest talking to a trusted friend or family member about becoming an authorized user.

Authorized users are people who have permission to use another person’s account but aren’t legally responsible for paying for the bill. This privilege is often given to children, spouses, and family members.

The original account holder has to agree to your authorization, and you can be removed at any time. If you are connected to someone’s account like this, you can benefit from their high credit score, as their credit line connects to yours.

You can buy authorized user credit lines online, but because of the intimate connection you will have with the other person’s financial details, we suggest asking a friend or family member first.

If you use the person’s credit card, or if they start to decline financially, then you will both see a dip in your credit score. If the authorized user doesn’t pay their bills and starts developing late payment fees, then the original card holder’s credit score will suffer.

Although this type of connection can be very helpful in increasing your credit score, both you and the original account holder have to think seriously about the commitment you are making before signing any contracts.

Get Credit For Rent

Despite rent being one of the biggest expenses in most people’s monthly budget, it isn’t rated highly on your credit score.

To make that big payment mean something to your credit history, you should pay the bill using a credit card and then pay the card back using your debit card.

The large payment to your credit card will show you using the credit line and being able to pay back a large sum of money with ease.

Make rent work for you.

Get Credit For Utility Bills

If you don’t pay for rent, then we suggest following the same logic with utility bills. Utility bills are counted in your credit score, which is why we wouldn’t suggest it normally, however they are another large payment you need to make.

Paying through your credit card, just like with rent, will show how you can pay back large sums of money with ease. Again remember that you should pay your credit card back almost immediately.

We suggest creating an automatic payment to the bill from the credit card, and another to the credit card from the debit card; always allowing for a couple of days’ wiggle room in case the banks take their time to make the payments.

Monitoring Your Credit Report

To maintain your good credit score, you need to know how credit scores are calculated. When you are aware of the 5 factors (payment history, amount owed, length of credit history, new credit lines, and credit mixes) you can use that knowledge to understand how your finances will be read.

If you monitor these credit details, you can manipulate your credit score into reflecting your best financial habits. Paying your bills on time, keeping your old credit cards, and keeping your credit balances as low as possible are all reachable goals to keep your credit score high.

Keeping an eye on your credit lines and credit report will help you notice when elements are slipping.

9TH ANNUAL PAPER SHREDDING EVENT

Clients, Friends & Neighbors, we would like to personally invite you to our 11th Annual Paper Shredding Event. We want to give back to our community by helping you get rid of unwanted documents. We are sponsoring File Keepers Shredding Company and Raffle prizes for our neighborhood. So Bring all of your documents to have the Disappear (shred) before your very eyes!

I look forward to seeing you there.

Home Downsizing Pros and Cons

There are many reasons to buy a smaller home—or to downsize from your present home—but sometimes, the idea that “less is more” is what propels homeowners to buy a smaller home.

When asked why they might want to purchase a smaller home, 69% of homeowners who have downsized in the past said saving money was their primary reason for doing so.1 But, of course, these reasons can vary.

While it’s true that we live in a society that often holds that “bigger is better,” it can be worthwhile to shift your thinking and consider whether a smaller home would actually serve you and suit your lifestyle.

Key Takeaways

- Downsizing can increase your cash flow, lower your utility bills, and reduce the time you spend on maintenance and upkeep.

- The downsides to downsizing include having less room for guests and having to get rid of belongings to fit into a smaller space.

- In general, it’s better to sell your current home before buying a new one, but discuss the possibilities with your agent for specific advice.

Potential Advantages of Downsizing

- Increased cash flow: If you’re spending less on your mortgage payment, you are likely to have money leftover every month to allocate for other needs or desires. Or perhaps you could pay cash for a smaller home from the proceeds of your existing home.

- More time: Fewer rooms and smaller spaces cut down on the time expended to clean and maintain. Smaller homes can reduce the time spent on household tasks, leaving more hours in the day to do something else more enjoyable. In fact, when asked about their primary reasons for downsizing, 36% of baby boomers, 18% of Gen Xers, and 19% of millennials said they did so because their previous homes were too difficult to maintain.1

- Lower utility bills: It costs a lot less to heat or cool a smaller home. Typically there is no wasted space, such as vaulted ceilings, in a smaller home. Less square footage decreases the amount of energy expended. Reducing energy is better for the environment and helps to keep your home green.

- Reduced consumption: If there is no place to put it, you’re much less likely to buy it. That means you may acquire less clothing, food, and consumer goods.

- Minimized stress: Less responsibility, smaller workload, increased cash flow, and greater flexibility—added together, they all reduce stress. Homeowners who have successfully downsized sometimes appear happier when they’re no longer overwhelmed by the demands of a larger home.

Potential Disadvantages of Downsizing

- Fewer belongings: Moving to a smaller home would probably result in selling, giving away, or throwing out furniture, books, and kitchen supplies. You’d have to sort through and empty out the garage, basement, and attic. Some people form emotional attachments to stuff and can’t part with any of it.

- No room for guests: Hosting a huge holiday dinner might be out of the question in a smaller home. Out-of-town guests might need to stay at a hotel when they come to visit.

- Space restrictions: Some homeowners report feeling cramped because there is less space in which to maneuver. It’s hard to get away from other family members and enjoy private, quiet time because there are fewer rooms to escape to when needed.

- Less prestigious: Sometimes appearances are more important than comfort levels. For homeowners who place a great deal of importance on how they are perceived by others, a smaller home might not project a coveted image of financial success.

- Lifestyle changes: Especially for long-term homeowners, trading down means changing a lifestyle, and some people are resistant to change. There is a certain comfort level obtained by staying with what is familiar.

Market Timing

The financial edge to downsizing, whether it’s a hot, cold, or neutral market, makes little difference overall. But one could argue that downsizing in a seller’s market would give the homeowner more cash on hand after closing. However, the trade-off could be a higher sales price for the smaller home.

For example, say in a neutral market that an existing home is worth $500,000, encumbered by a $200,000 mortgage. Not counting closing costs, which may include commission and title fees, the net proceeds would be $300,000. Let’s also assume that a seller could buy a smaller home for cash at $250,000, putting $50,000 in the pocket.

If it’s a seller’s market, however, and prices have jumped 10%, the existing $500K home might be worth $550,000. Meaning the smaller $250K home could be purchased at $275,000 in cash, resulting in $75,000 cash remaining.

If it’s a buyer’s market, say, and prices have fallen 10%, then the existing home could be worth $450,000. The smaller $250K home would be priced at $225,000, resulting in $25,000 cash to put in the bank.

The best of both worlds would be to sell in a seller’s market and buy elsewhere in a buyer’s market. Either way, a seller could end up owning a free-and-clear smaller home, so take your pick of markets. Realize, though, that you can’t really time the market.

Buy or Sell First?

Sellers often ask whether they need two agents to buy and sell. First, consider similar comparable sales and your home pricing. Second, is it located in a neighborhood where out-of-area agents are shunned by local agents? It’s not supposed to happen, yet it does. But if your home is easy to price, and the agent has contacts in that area, it doesn’t really matter where the agent is located. Sometimes agents will negotiate the commission if they are handling two transactions.

Should you sell first and then buy, or buy first and then sell? Generally, it’s better to sell your existing home before buying a new home. The reason is it keeps your emotions in check. But some markets will dictate that it’s better to buy before you sell. Discuss this strategy with your real estate agent.

Article by ELIZABETH WEINTRAUB

Elizabeth Weintraub is a nationally recognized expert in real estate, titles, and escrow. She is a licensed Realtor and broker with more than 40 years of experience in titles and escrow. Her expertise has appeared in the New York Times, Washington Post, CBS Evening News, and HGTV’s House Hunters.Learn about our editorial policies

Homeowners Insurance and Tree Damage

As a homeowner, it’s your job to care for and protect your property, but home insurance companies offer policies that can help you with the protection part. Tree damage may not be the first thing that comes to mind when choosing coverage levels for your homeowner’s insurance, but if a tree falls on your home, it can damage your house and your possessions and cause financial devastation. The endless ‘what if’ scenarios can feel overwhelming, but as far as tree damage is concerned, it’s best to pick coverage rooted in caution and practicality.

Much like the Lorax speaks for the trees, we’ve outlined preventative measures you can take to care for or remove trees and protect your property from tree damage. We’ve also outlined scenarios where your home insurance might or might not cover damage caused by trees. Understanding the nuances of a standard homeowners insurance policy could help ensure you know what is covered if a tree wreaks havoc on your property and what damage you might be responsible for out of pocket.

On this page

Key statistics

- 2% of homeowner’s insurance losses were caused by property damage in 2019. Over a third of that property damage was due to natural causes, specifically wind and hail. (Insurance Information Institute (Triple-I)

- Insurance companies paid an average of $4,110 for settled tree claims. Seven percent of these claims were as a result of a fallen tree. (Consumer Reports)

- If a tree located on your neighbor’s property damages your house or property, your insurance company may try to collect from their insurance company. If successful, you could be reimbursed for your deductible. (Triple-I)

- If you have particularly valuable trees on your property, you should consider how much it would cost to replace them when determining how much homeowners insurance you need. (Triple-I)

- Standard homeowners insurance typically covers damages to trees and shrubs due to disasters or accidents like fire, lightning, vandalism and theft, but this coverage is typically limited to five percent of the amount of insurance on the structure of your home, and insurers will also usually cap coverage for any one tree, shrub or plant. (Triple-I)

Does homeowners insurance cover tree damage?

Whether or not a homeowners insurance policy covers tree damage depends on the situation. In order for the damage to be covered, the cause of the tree falling must be due to a covered peril. Many homeowners know they can usually file a claim if a tree damages a covered structure, but you may not know that many home insurance policies also cover at least some portion of damage to the actual trees, shrubs or plants, as long as the damage was caused by a covered peril.

So if a tree falls in your yard but does not damage your home or any other structure on your property, some portion of it may be covered by your home insurance policy. According to the Triple-I, this type of coverage will generally be capped at a certain percentage of your dwelling coverage limits. It’s important to note that most home insurance companies will not pay for tree or shrub removal, except in some cases where it is blocking a driveway or handicap access.

Every policy is different, however, so you should consider speaking with your insurance agent about what is and is not covered in your policy — before tree damage occurs.

Tree damage causes typically covered by home insurance:

- Storms

- Hail

- Ice

- A fire caused by lightning (and other apocalyptic events)

Tree damage causes typically not covered by home insurance:

- Rot

- Age

- Flood

- Earthquake

Does homeowners insurance cover tree removal?

Homeowners insurance typically covers the removal of trees if they have fallen due to a covered peril and onto a covered structure, like your house, or if the tree is blocking an access point. Some situations where tree removal may be covered are:

- If a tree falls on an insured structure, such as your home itself or a garage

- If a fallen tree is blocking a driveway

- If a fallen tree is blocking a handicap-accessible ramp

Situations where tree removal is not covered under your insurance policy should be carefully considered. If your home hasn’t been damaged by a fallen tree, but you want to preemptively remove trees on your property, it is unlikely to be covered — and could even have negative consequences.

For example, if the person responsible for removing the tree is injured during the process, you may risk legal repercussions as the property owner. Bodily injury liability is one of the more infrequent causes for insurance claims, but can be one of the most costly. From 2015-2019, according to the Triple-I, bodily injury and property damage was the second severest homeowner’s insurance claim, costing an average of $29,752.

Insurance companies consider your justification for tree removal to determine if it will be covered. They will likely not cover the removal if you’re worried about your yard aesthetic and find the tree unsightly. If an insured structure was hit, insurance providers may reimburse you for tree removal up to a specified dollar amount, usually ranging from $500-$1,000. If a covered structure was not hit, your insurance company is unlikely to pay for its removal, except, possibly, in the circumstances mentioned above. It’s important to check your policy and ask your agent to determine your exact coverage.

What to do when someone else’s tree damages your property

A standard homeowners insurance policy should cover a tree that falls on your house, regardless of who owns the tree.

In some cases, the insurance company may try to collect the money needed to cover the damage from the neighbor’s insurance company in a process called subrogation, which may also cover the deductible for the homeowner whose property was damaged.

However, if your neighbor’s tree has not fallen on your house, but it’s encroaching on your property, do you have the right to cut it?

Usually, it depends on whose yard has the tree trunk. If your neighbor’s tree branches and leaves cover portions of your yard, but the tree trunk is in his yard, it belongs to your neighbor. In that case, your local laws or HOA governance will likely determine whether overgrown trees that encroach on your property must be maintained by their owner.

Tree removal in these cases can lead to disputes between you and your neighbors who have differing opinions on the matter. Your HOA may get involved, or worse — your neighborhood Facebook page could become the battleground for the tree removal debate.

Another risky ‘what if’ is if your tree is damaging your neighbor’s property. It could cost you and your insurance provider to compensate for the damages, not to mention your reputation in the neighborhood. That’s why regular care and maintenance of your trees is typically a good idea.

How much to expect from the insurance company

The payout from your insurance company after tree damage depends on several factors, including what type of property was damaged. If a covered peril causes damage to your house, you may be eligible to receive up to the limit of your policy’s dwelling coverage, depending on how much damage was done.

You can usually also file a claim for your personal belongings, if they were damaged, up to certain limits. Different categories of possessions have individual limits and high-value items may not be covered at all, unless you have added them with scheduled personal property insurance. You can choose to increase these limits, but it will likely cause your homeowners insurance premium to go up.

How much you are reimbursed for your belongings and dwelling coverage also depends on whether you have actual cash value (ACV) or replacement cost value (RCV) on your policy.

If the tree itself that caused damage to your home was valuable, you might also be able to file a claim to replace it. As mentioned earlier, not all policies will cover the actual tree, and the ones that do will likely have certain coverage caps in place, so you will need to look at your policy or speak with an agent to see how much is covered.

Once a claims adjuster creates an estimate for each claim category, the insurance company subtracts your policy deductible from the amount you receive. Many homeowners insurance policies also cover some living expenses, such as hotels, up to certain limits if your home is uninhabitable while the damage is repaired.

How to prevent tree damage

It is your responsibility as a homeowner to maintain your trees properly. Damage caused by dead or rotting trees is not likely to be covered by homeowners insurance, and if a tree owned by you causes damage to someone else’s property or person, you might get sued. Here are a few things you can do to prevent trees from causing damage to structures and property:

- Trim any trees on your property regularly, especially those with long branches.

- Check for signs your trees are dead or dying (not on Healthline) by observing a year-round lack of leaves or hollow trunks.

- Look for mushrooms, cracks or holes at the base of tree trunks to rule out rotting.

- Consider removing trees that are leaning off-center that have a higher potential to fall.

- Pay extra attention to trees that hang over your roof, driveway or power lines.

- Consider having a tree expert examine the trees on your property periodically to look for signs or disease or rot, or to recommend preventative maintenance.

Frequently asked questions

What is the best home insurance company?

Finding the best home insurance company depends on a lot of factors. It is a good idea to compare quotes from some of the top home insurers in the country using criteria like customer service scores from J.D. Power, financial strength ratings from AM Best and average premiums. Not every homeowner has the same needs, so it is smart to look at several options and speak with a licensed insurance professional.

Does homeowners insurance cover diseased tree removal?

Diseased tree removal is generally considered routine maintenance and is not typically covered by a standard homeowners insurance policy. It is your responsibility to track the health of your trees and treat them when needed.

If a falling tree damages my roof, will that be covered by homeowners insurance?

A roof can be expensive to replace, but most standard policies will cover tree damage to a roof if the following perils caused it:

- Fire or lightning

- Windstorms and hail

- Explosions

- Riots, vandalism or theft

- Damaged caused by aircraft or vehicles

- Smoke

- Volcanic eruptions

- Falling objects

- The weight of snow, ice or sleet

In most cases, roof damage from a tree felled by floods or earthquakes is not covered. It is a good idea to purchase a separate policy to cover these perils if you live in an area prone to either. Note that insurance companies will typically only cover your roof if it is in good repair. If you are unsure of the specific coverages included in your policy, turn to your agent or insurance company for clarification.

Do trees add value to my home?

Arbor Day Foundation finds that planting trees in residential areas can increase property values anywhere from three to 15 percent. Trees can really spruce up a neighborhood and appeal to potential buyers.

Removing dying or rotting trees can also increase the value of your home by eliminating that risk for future residents, according to Realtor.com. Remember that the cost of removing trees, even if diseased or rotting, is considered routine care and maintenance and is usually not covered by insurance.

What types of trees are the safest?

It’s typically a good best practice to select trees that don’t forget their roots — literally. If you’re considering planting a tree or evaluating the type of tree on a property you’re looking to buy, look for healthy, strong roots. Bonus points if the tree is relatively low-maintenance.

Some of the best trees for this can include oaks, maples, hickories and elm trees, according to Realtor.com. You might want to consult with a landscape expert to determine what trees are the best for your climate and property type.

What types of trees can’t be trusted?

Simply put, trees that ain’t from ‘round these parts are better avoided. Experts advise picking trees best-suited for your environment and considering their native location. For example, non-native tree types like black locusts and box elders, native to the Southeast and Central/East regions, generally wouldn’t thrive in the desert climate of the Western U.S., according to Realtor.com.

It’s also usually a good idea to avoid trees that attract invasive species of insects or trees with invasive roots. These types of trees can bring unwelcome visitors to your home or shift the foundation of your house entirely.

Trees with these types of roots include willows, hybrid poplars and silver maples, all of which have the potential to invade your sewer lines and drain pipes.

Again, speaking with an ISA Certified Arborist or landscape professional might be the best idea to determine what trees are right for your home.

Read more From Lauren Lauren Ward has nearly 10 years of experience in writing for insurance domains such as Bankrate, The Simple Dollar, and Reviews.com. She covers auto, homeowners, and life insurance, as well other topics in the personal finance industry.

Original Article Posting: https://www.bankrate.com/insurance/homeowners-insurance/does-homeowners-insurance-cover-fallen-trees/

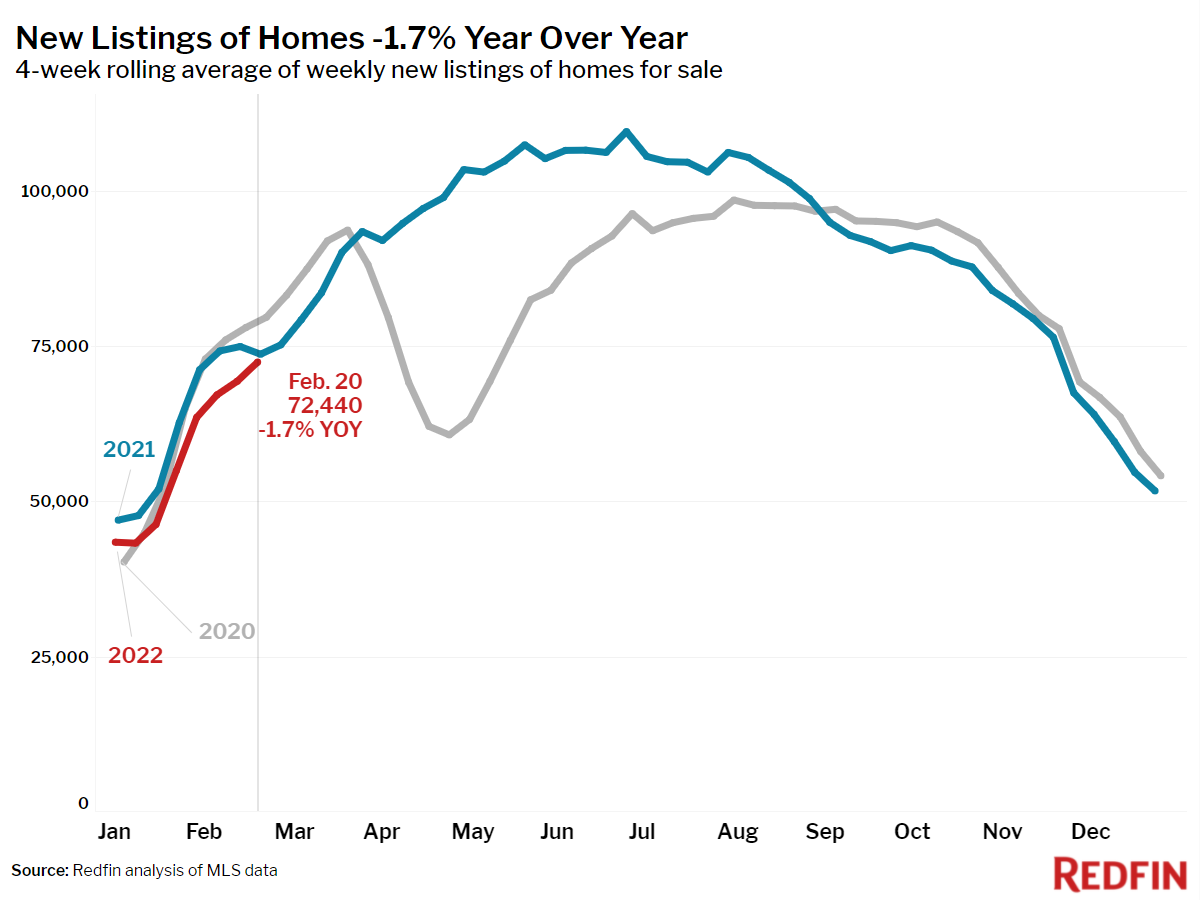

Housing Market Update: New Listings Gain Steam, Met by Hearty Demand

New listings post smallest year-over-year decline since mid-November; pending sales rise 1%.

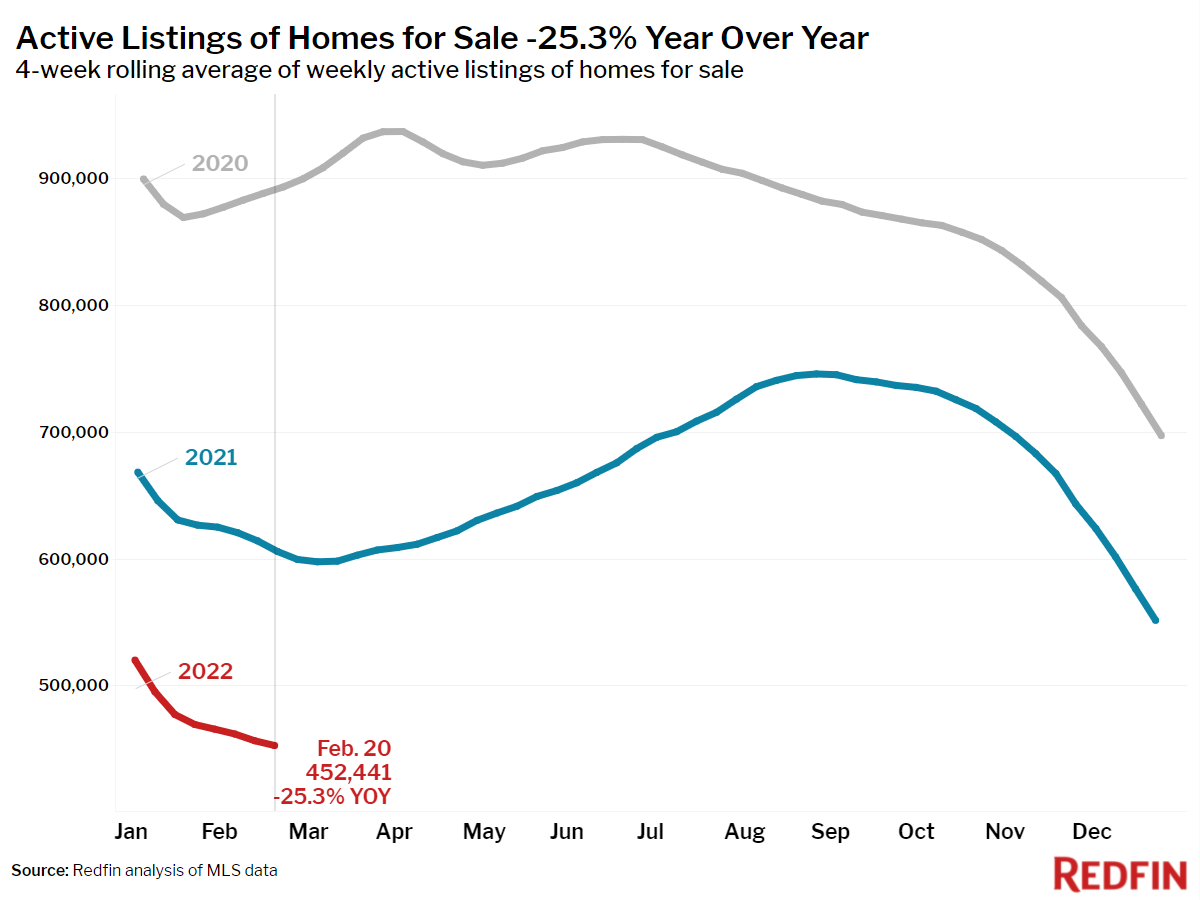

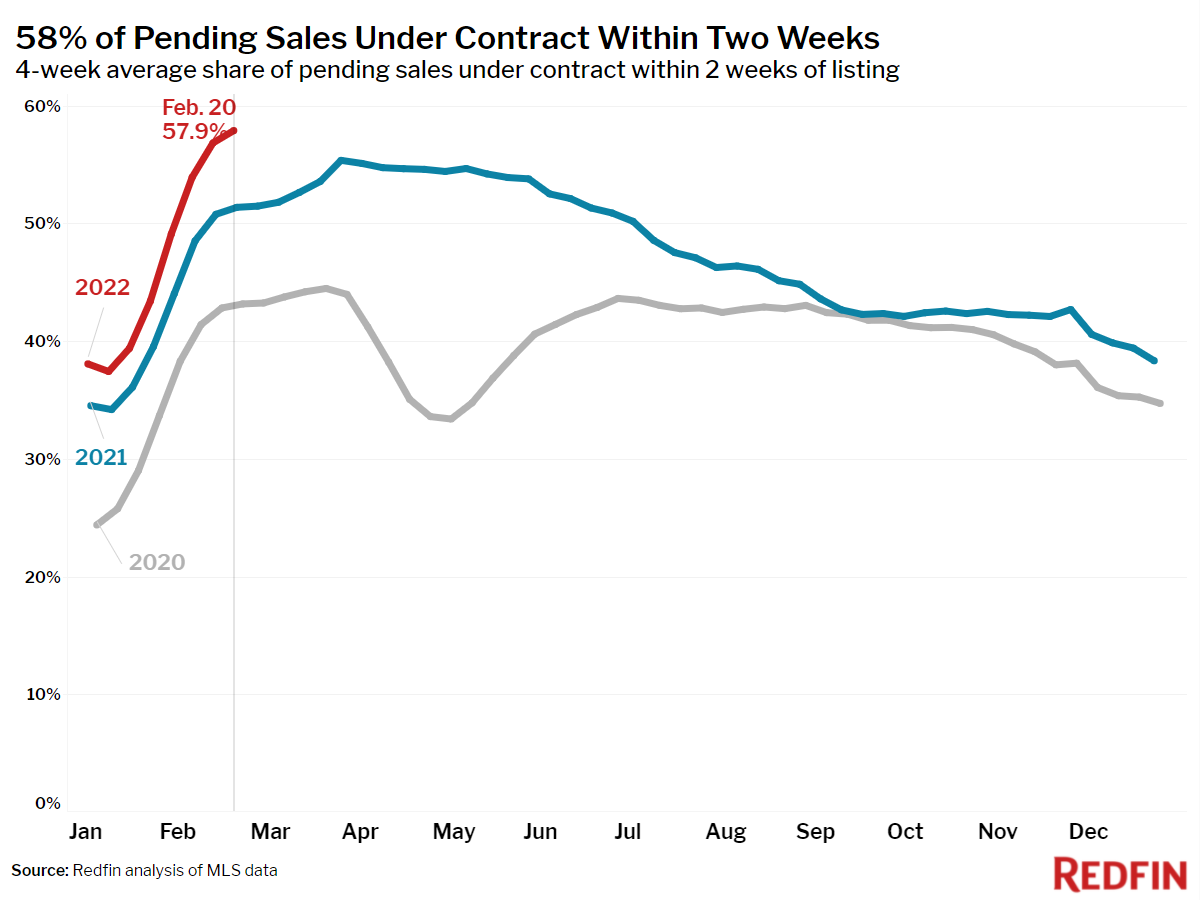

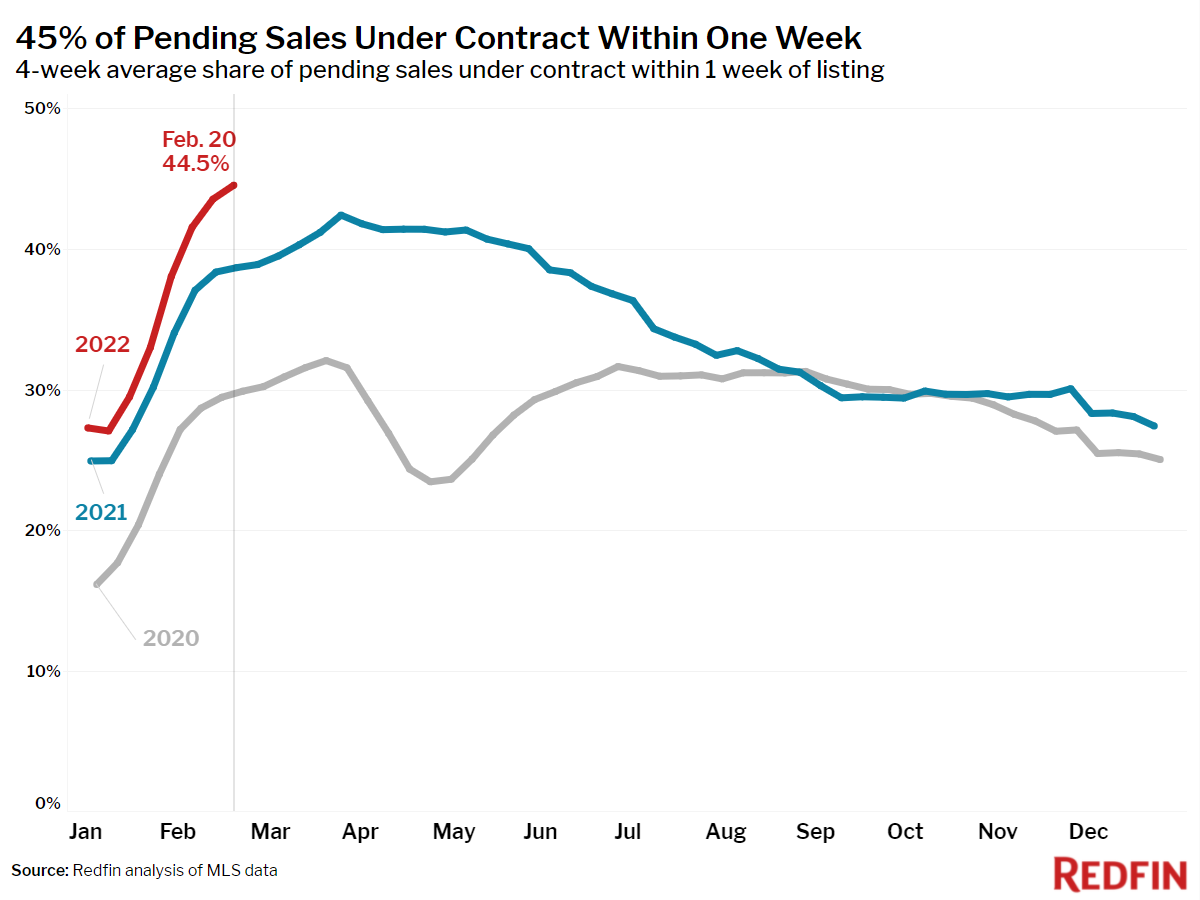

Home-selling activity is finally gaining some steam. The number of homes newly listed for sale during the four weeks ending February 20 was down just 2% year over year, the smallest decline since mid-November. More new listings were met with hearty demand. Pending sales rose 1%, the first increase since mid-January. The market again set new record highs for home sale prices, asking prices, buyers’ mortgage payments and the share of homes selling within days of hitting the market. We also saw a new all-time low for the total number of homes for sale.

”The good news for homebuyers is that each week more homes are being listed for sale,” said Redfin Deputy Chief Economist Taylor Marr. “There is growing evidence that January’s dramatic drop in new listings was only a temporary blip driven by heavy winter storms and the spike in Covid cases, so homebuyers may have some hope for better selection in the coming spring season.”

Key housing market takeaways for 400+ U.S. metro areas:

Unless otherwise noted, the data in this report covers the four-week period ending February 20. Redfin’s housing market data goes back through 2012.

Data based on homes listed and/or sold during the period:

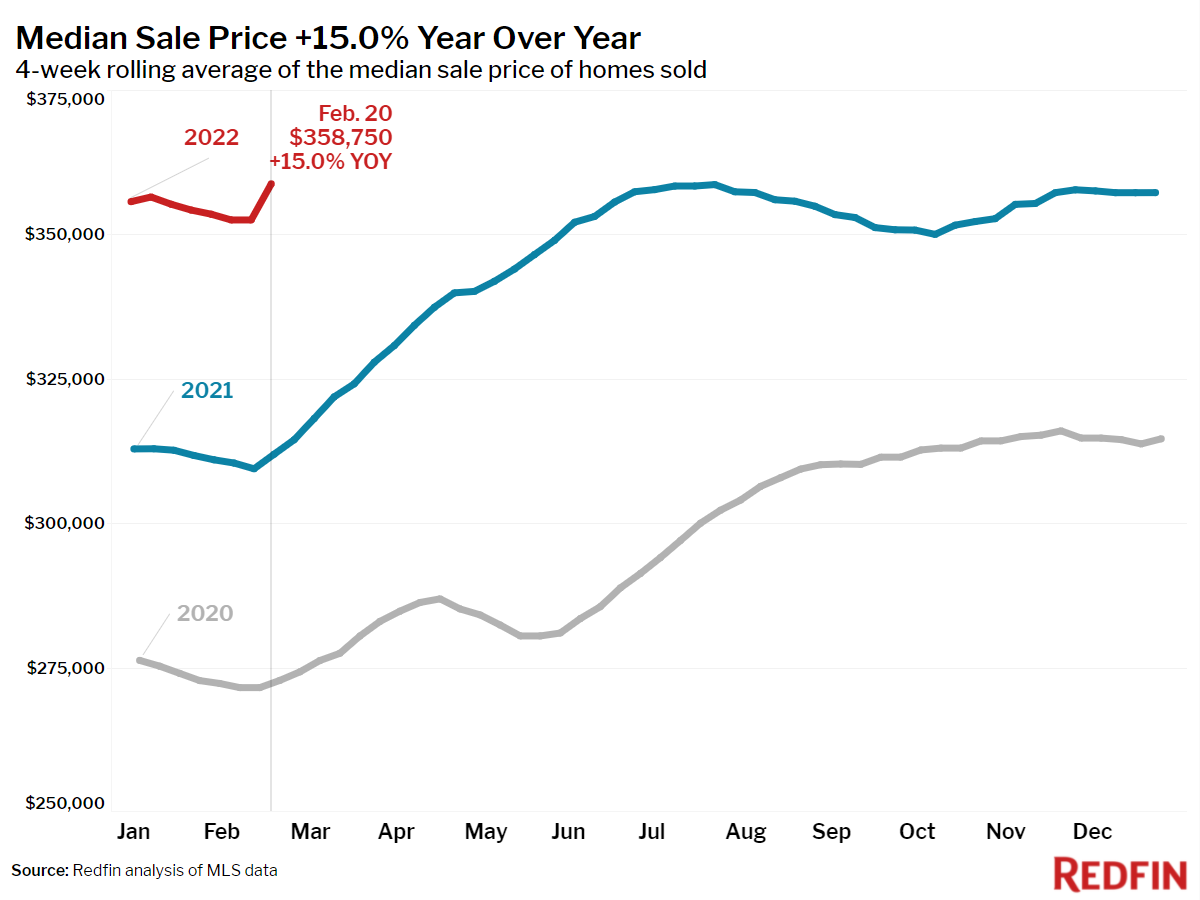

- The median home sale price was up 15% year over year to a record high of $358,750. This was up 32% from the same time in 2020.

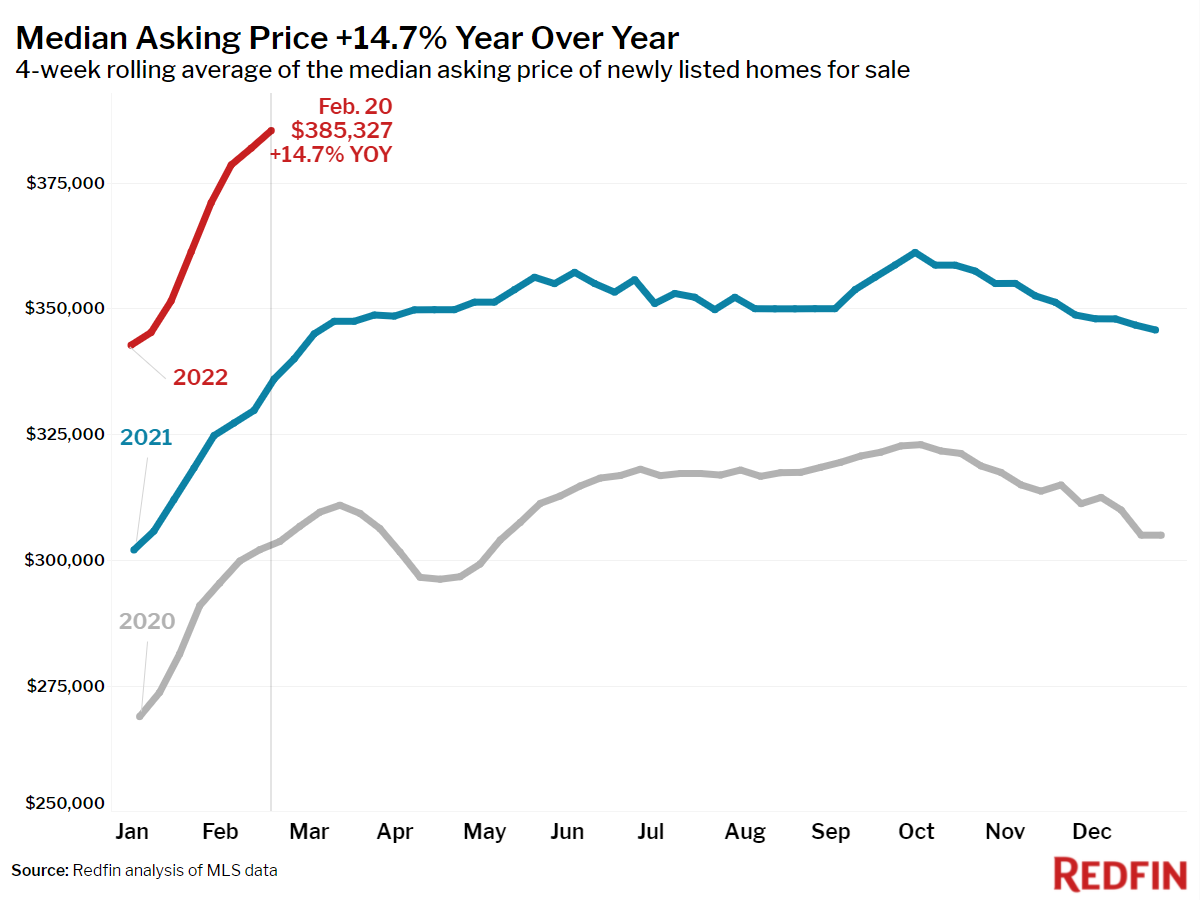

- The median asking price of newly listed homes increased 15% year over year to an all-time high of $385,327. This was up 27% from the same time in 2020.

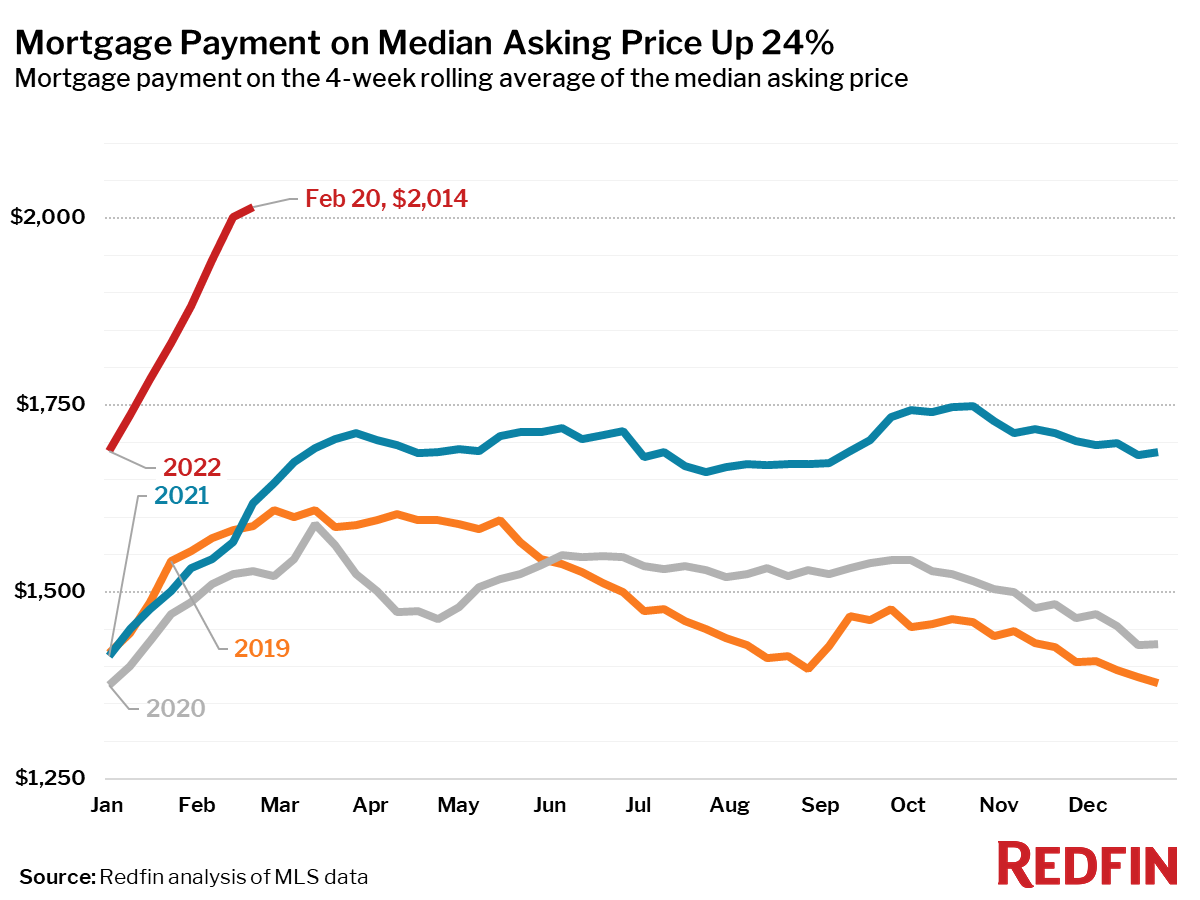

- The monthly mortgage payment on the median asking price rose to an all-time high of $2,014. This was up 24% from a year earlier when mortgage rates were 2.97%, and was up 34% from the same period in 2020 when rates were 3.45%.

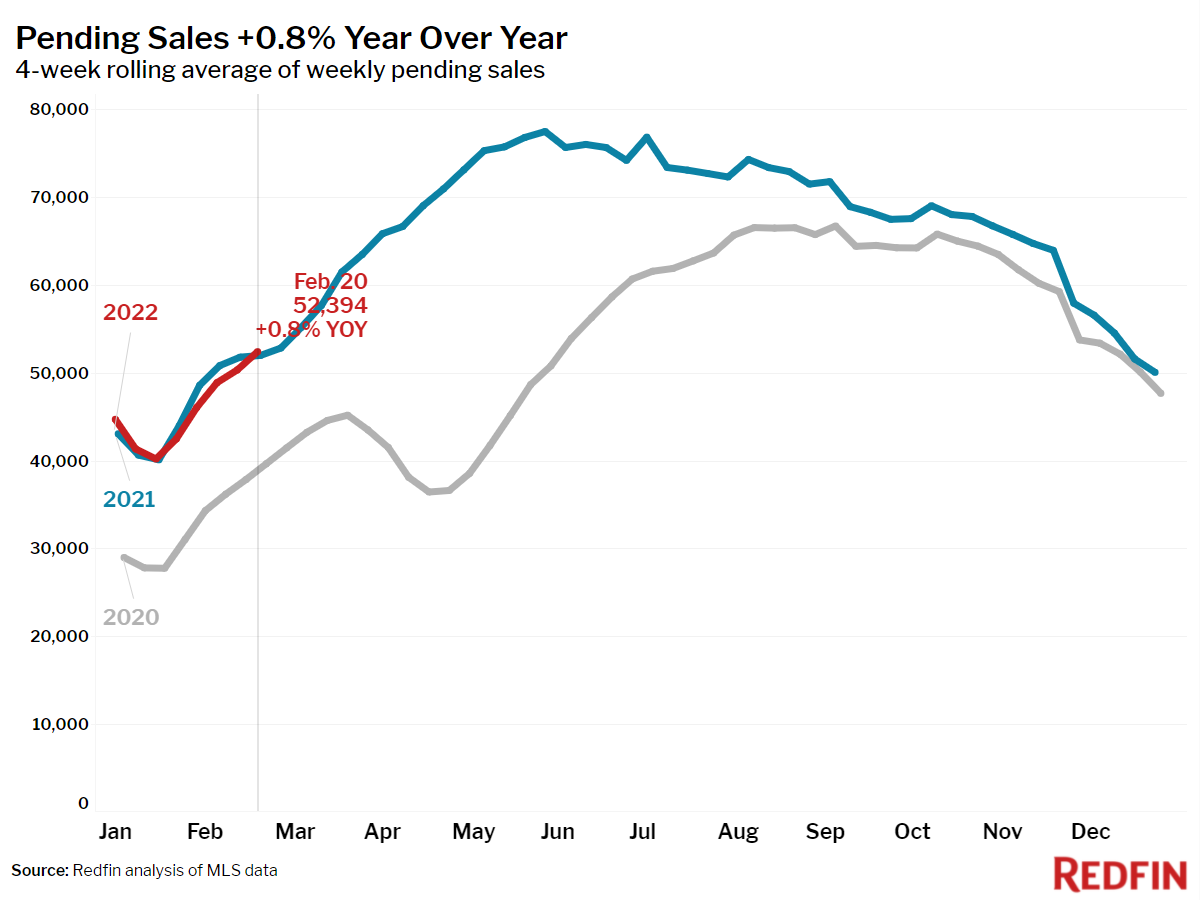

- Pending home sales were up 0.8% year over year, the first increase since the four-week period ending January 16. Sales were up 32% from the same period in 2020, just prior to the start of the pandemic.

- New listings of homes for sale were down 2% from a year earlier. This was the smallest decline since the four-week period ending November 14. Compared to 2020, new listings were down 9%.

- Active listings (the number of homes listed for sale at any point during the period) fell 25% year over year, dropping to an all-time low of 452,000. Listings were down 49% from the same period in 2020.

- 58% of homes that went under contract had an accepted offer within the first two weeks on the market, an all-time high. This was up from the 51% rate of a year earlier and 43% in 2020.

- 45% of homes that went under contract had an accepted offer within one week of hitting the market, an all-time high. This was up from 39% during the same period a year earlier and 30% in 2020.

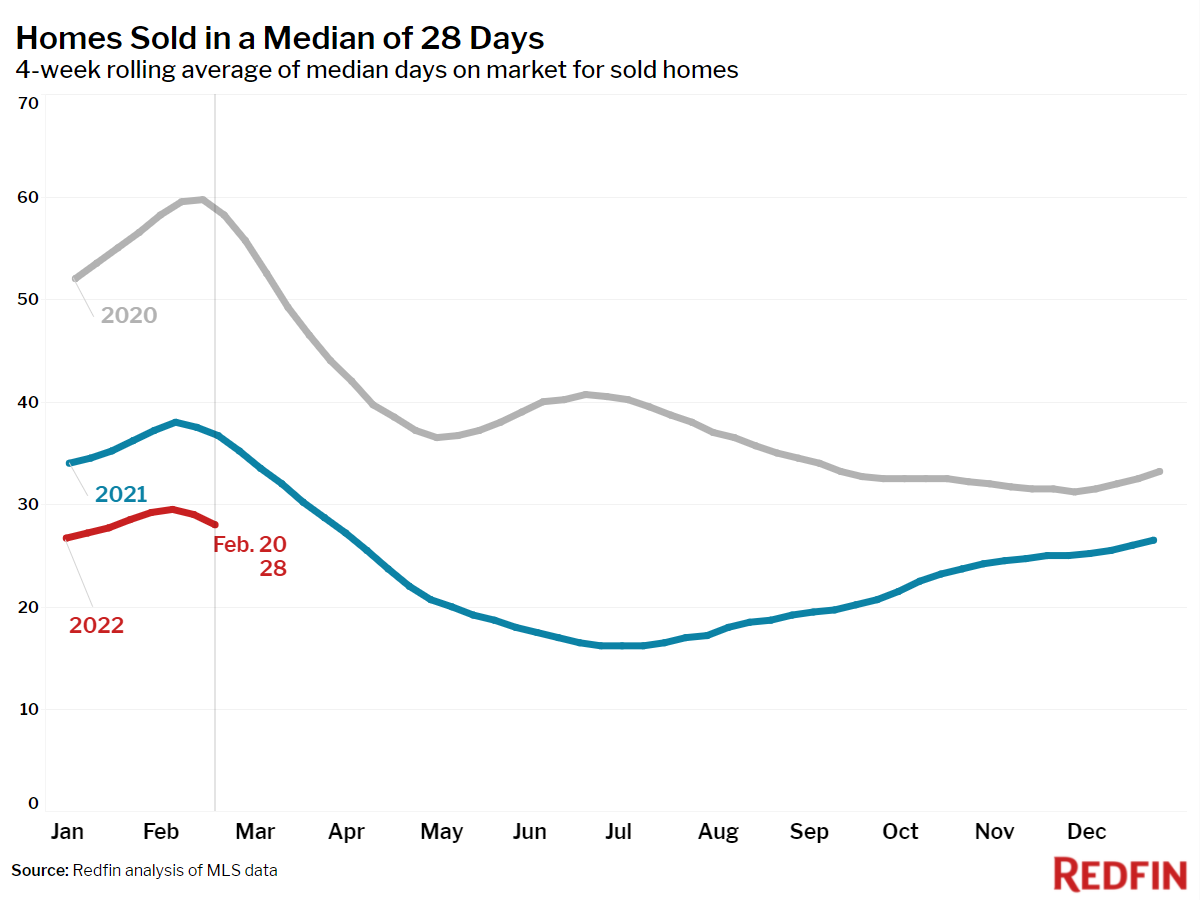

- Homes that sold were on the market for a median of 28 days, down from 37 days a year earlier and 58 days in 2020.

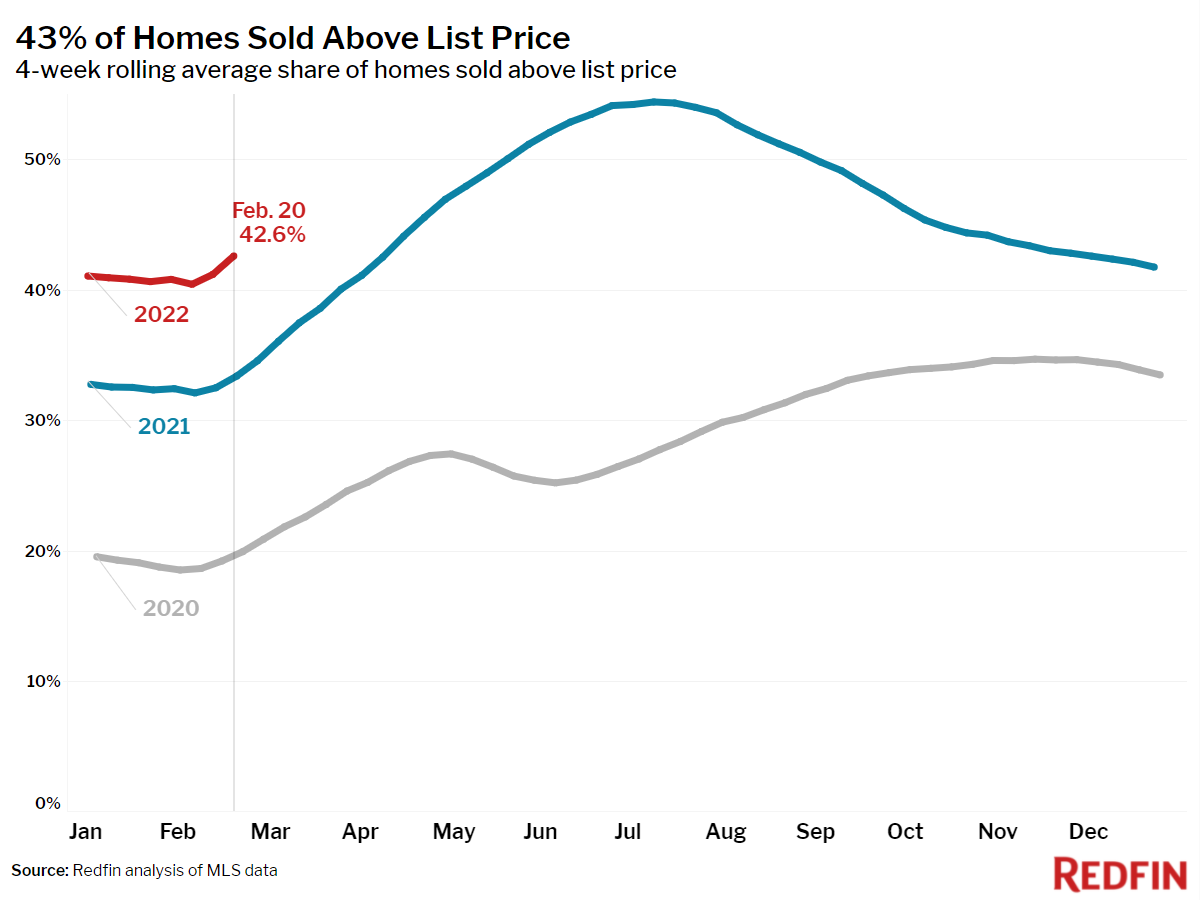

- 43% of homes sold above list price, up from 32% a year earlier and 20% in 2020.

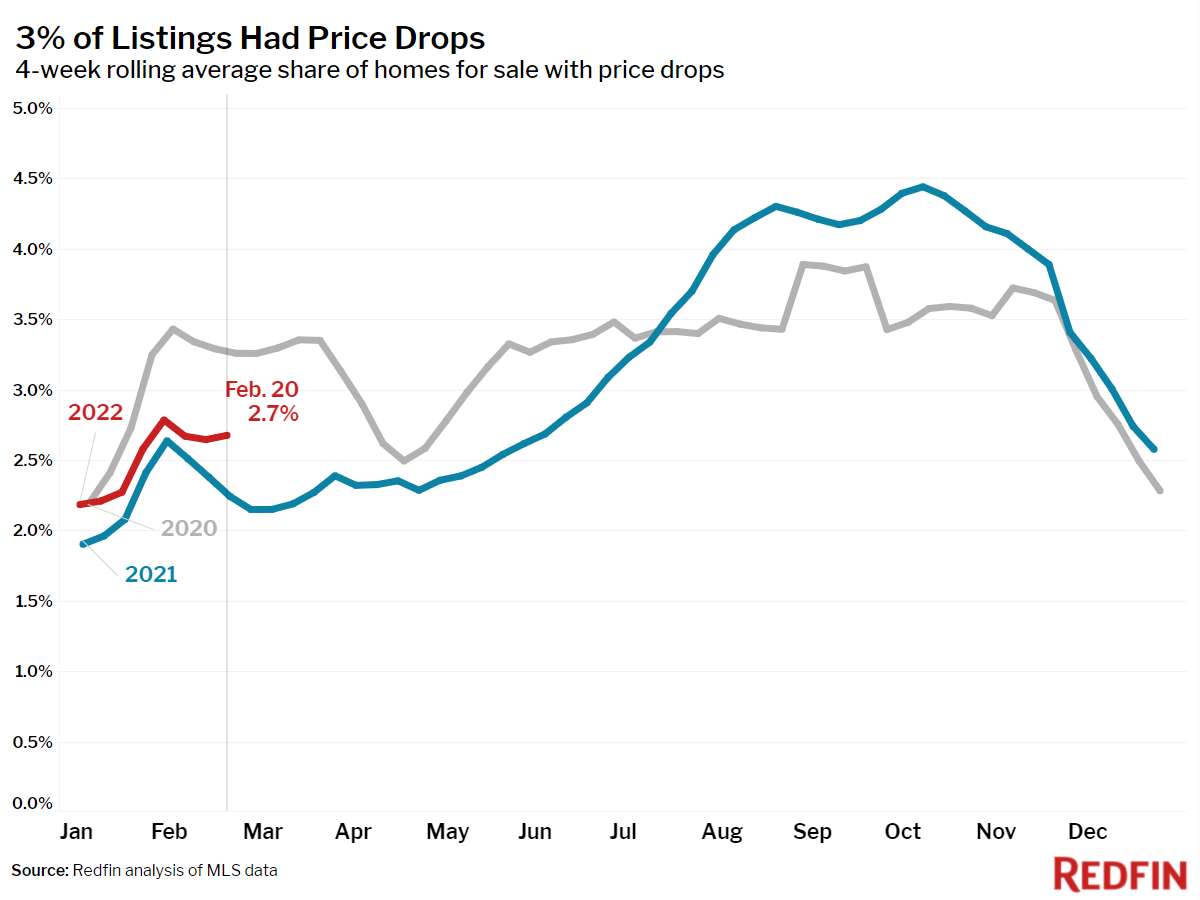

- On average, 2.7% of homes for sale each week had a price drop, up 0.4 percentage points from the same time in 2021, but down 0.6 percentage points from 2020.

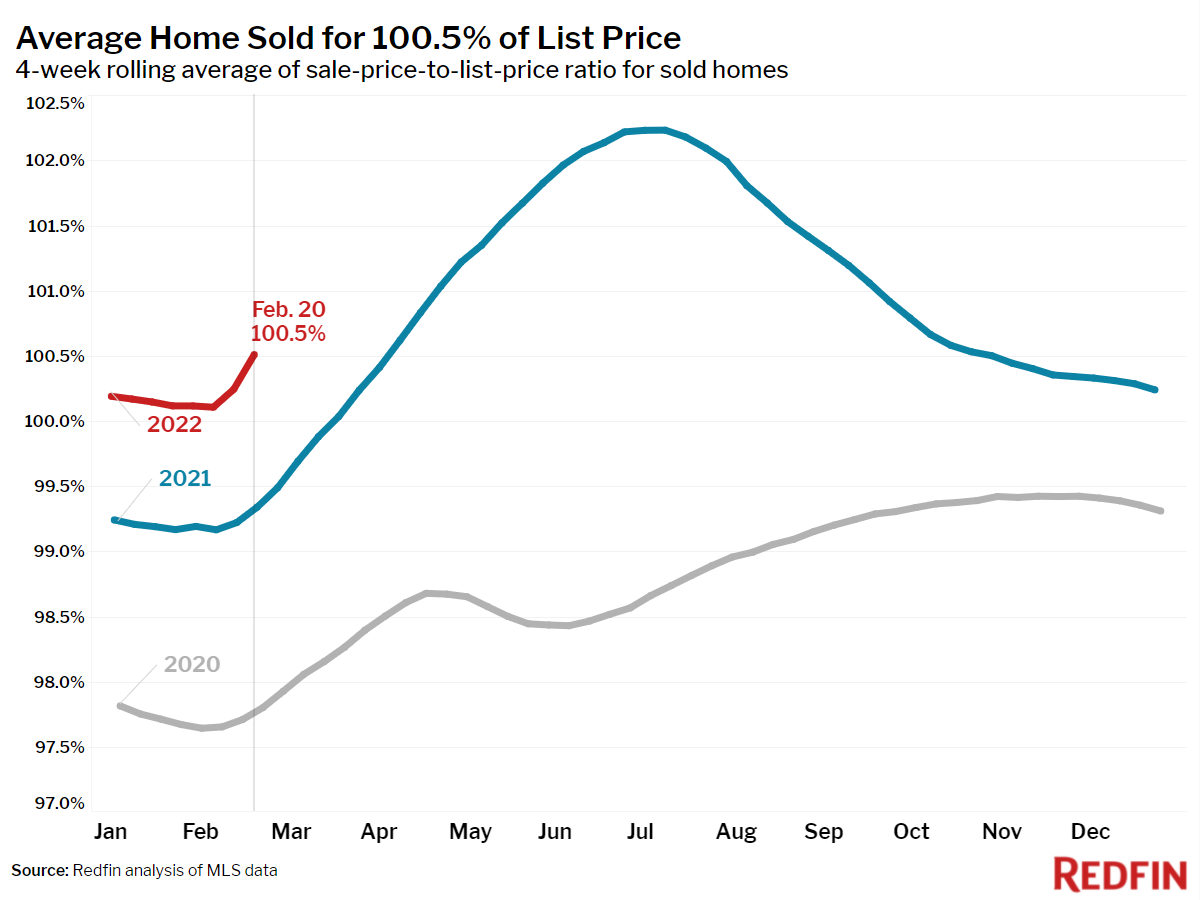

- The average sale-to-list price ratio, which measures how close homes are selling to their asking prices, rose to 100.5%. In other words, the average home sold for 0.5% above its asking price.

Other leading indicators of homebuying activity:

- Mortgage purchase applications decreased 10% week over week (seasonally adjusted) during the week ending February 18. For the week ending February 24, 30-year mortgage rates fell slightly to 3.89%, the highest level since May 2019.

- Touring activity through February 20 was 17 percentage points ahead of 2021 and 2 points behind 2020 relative to the first week of January according to home tour technology company ShowingTime.

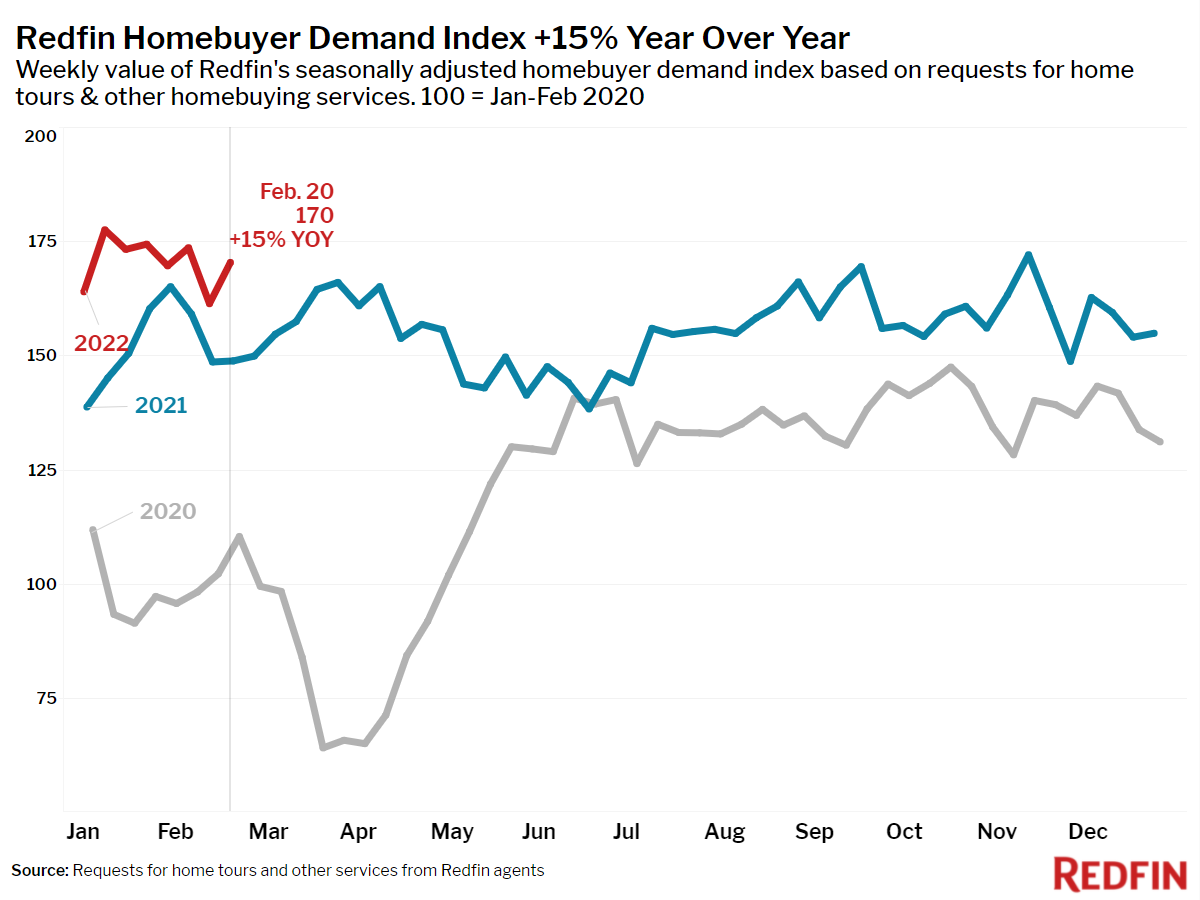

- The Redfin Homebuyer Demand Index rose 6% during the week ending February 20 and was up 15% from a year earlier. The seasonally adjusted Redfin Homebuyer Demand Index is a measure of requests for home tours and other home-buying services from Redfin agents.

Refer to our metrics definition page for explanations of all the metrics used in this report.